Selected Student Research

|

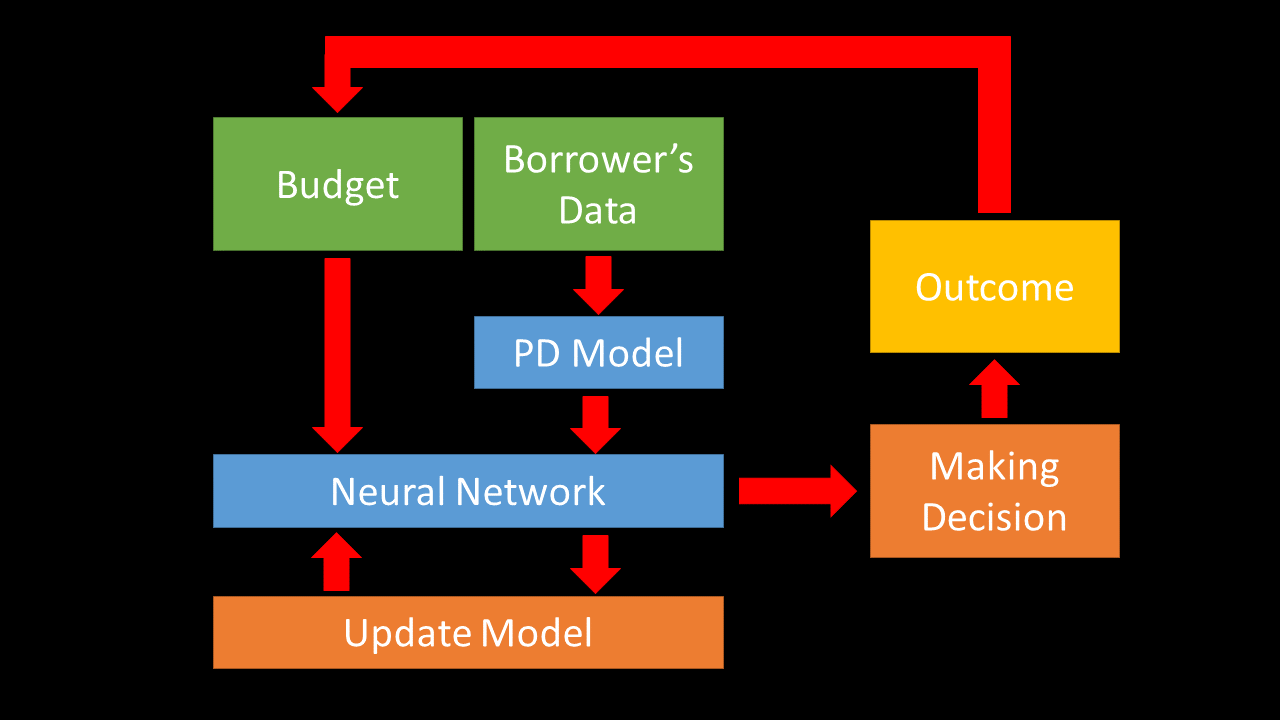

A Reinforcement Learning Model for Lending Problems with Limited Budget and Insufficient DataTraditional lending policy requires sufficient data for making lending decisions, therefore, some small companies could not access to the fund. In this study, we propose a decision making model that can decide whether to accept or reject a sequence of unfamiliar loan applications while having a limited budget. Our model does not have any knowledge about the incoming loans, therefore, it can predict the default probability with low accuracy at the beginning. The model can learn by observing the outcomes of the accepted loans. The model’s budget increases every time the model accepts a fully paid loan and decreases when the model accepts a defaulted loan. The objective of our model is to maximize the final budget. By using the reinforcement learning method, we propose a decision making model that takes the current budget and model accuracy into consideration when making decisions. Based on simulated data, the results show that our model yields a better performance compared to a traditional default prediction model. For the real data, our model performs well in some type of loans.

|

|

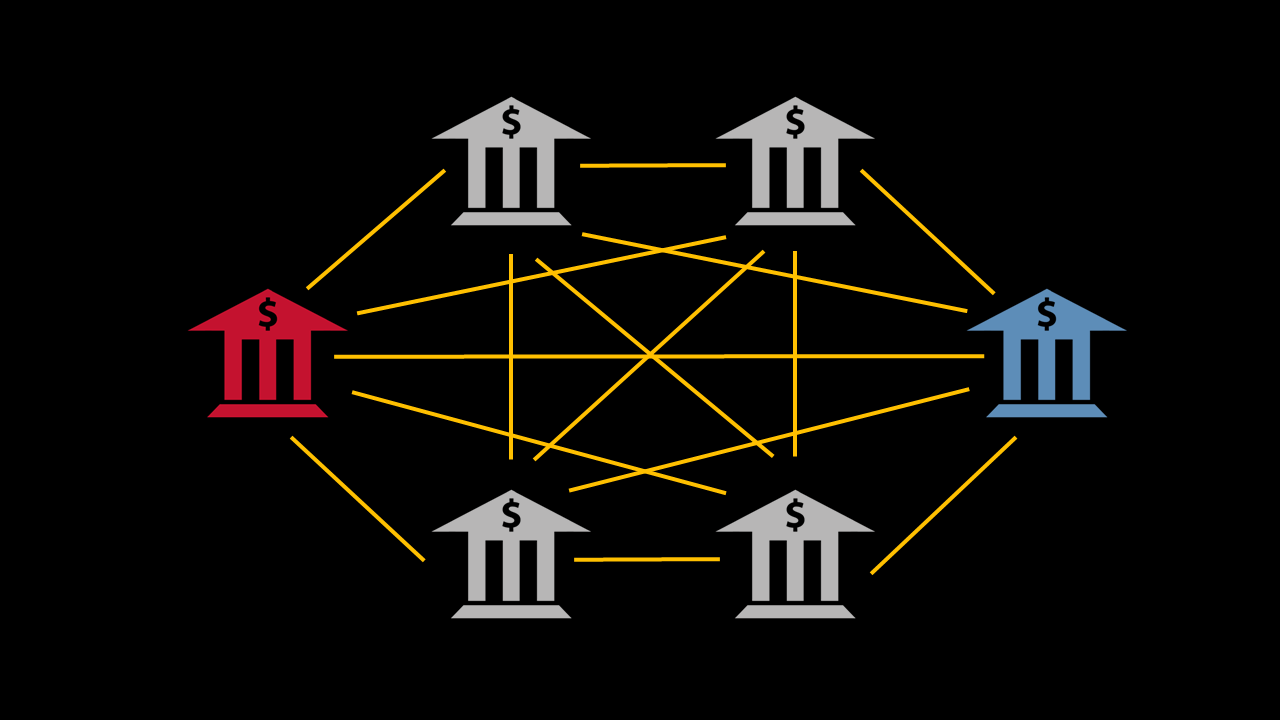

Bank Characteristics and Financial Contagion through Interbank Liability and Market ChannelsIn this research, we model the systemic risk in a banking system using an equilibrium approach where banks in the financial system are risk averse and aim for optimal illiquid asset holdings. Contagion can occur through interbank lending and changes in the asset price. We show that in the face of financial contagion, the incomplete financial system, such as a ring topology, that keeps banks with greater risk aversion coeffcients away from loss can amplify a fire-sale effect as they contribute low level of demands toward the market and act as poor buyers. In contrast, in a highly interconnected financial system such as complete and star topologies, banks with greater risk aversion coeffcients, instead, become more useful as shock absorbers and thus, soften a fire-sale effect. On the other hand, the incomplete financial system, such as a ring topology, that keeps banks with low risk aversion coeffcients away from loss can help soften a fire-sale effect as they are able to contribute high level of demand toward the market. In contrast, a highly interconnected financial system, such as complete and star topology, instead, renders banks with low risk aversion coeffcients less supportive as potential buyers as they reduce their demand more intensely due to the transmitted loss, and hence amplifying the fire-sale effect. Our results thus highlight that the same risk averse banks that contribute to resilience under certain financial systems may function as significant sources of fire-sale effect under others.

|